Financial freedom is a term that many people dream of, but few truly understand. In simple terms, financial freedom means having enough wealth and income to live your life on your terms without the constant need to rely on a paycheck. It’s about not worrying about money or living paycheck to paycheck. You can pursue what you love, spend time with your family, and enjoy life without stressing about finances.

“A big part of financial freedom is having your heart and mind free from worry about the what-ifs of life” – Suze Orman

But how does someone in India reach this point? What practical steps can you take, and what mindset do you need to develop? This guide will walk you through how to achieve financial freedom in India, sharing proven strategies, money-saving tips, and smart investment advice. Whether you’re just starting out or already managing your finances, you’ll learn exactly how to save money in India and build long-term wealth. By the end, you’ll be ready to take control of your finances and confidently move toward true financial independence.

What is Financial Freedom?

Before we dive into the details of how to achieve financial freedom, it’s essential to define what it means. Financial freedom can be different for everyone. For some, it might mean retiring early, while for others, it could mean having the ability to work for passion rather than money.

At its core, financial freedom is the state where your passive income or investments generate enough money to cover your living expenses. This means you don’t have to depend on your salary or wage to make ends meet.

For many Indians, financial freedom is an attractive goal. With rising inflation, unpredictable job markets, and increasing living costs, the need for a stable financial future has never been greater.

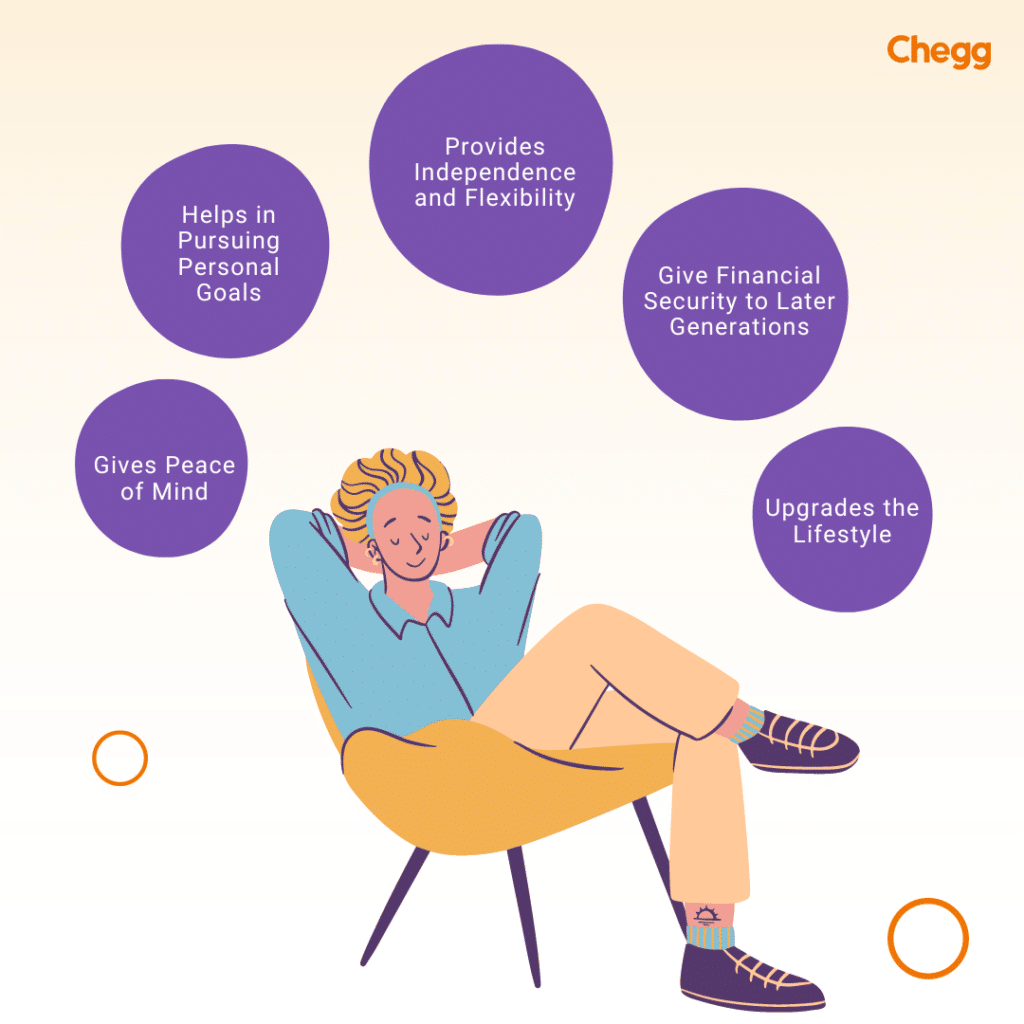

Why is Financial Freedom Important?

India is rapidly evolving, and so are its financial challenges. The cost of living in major cities like Mumbai, Delhi, and Bangalore continues to rise, while salaries in many industries are not growing at the same pace. This means that many people are finding it harder to save or invest for their future.

Achieving financial freedom in India can offer you several benefits:

- Security and Peace of Mind: Financial freedom reduces anxiety about unexpected expenses or job losses.

- More Opportunities for Growth: With financial freedom, you can explore new opportunities, whether in business, education, or personal development.

- Enjoy Life on Your Terms: Once you achieve financial independence, you have the freedom to choose how you spend your time, whether it’s traveling, pursuing hobbies, or spending time with family.

How to Achieve Financial Independence in India: A Step-by-Step Guide

Achieving financial freedom is not a quick process. It requires discipline, planning, and a willingness to make smart decisions. Here is a 7 steps to achieve financial freedom to help you along your journey.

1. Assess Your Current Financial Situation

The first step towards financial freedom is understanding where you stand financially. This means assessing your income, expenses, assets, and liabilities. By doing this, you can get a clear picture of your financial health.

- Track Your Income and Expenses:

- Start by tracking all your sources of income, such as your salary, business income, or freelance earnings.

- Then, note down all your monthly expenses. This includes rent, utilities, groceries, insurance, transportation, and entertainment.

- Calculate Your Net Worth:

- List all your assets, including savings, investments, and properties.

- Subtract any liabilities, such as loans, credit card debt, and mortgages.

- Identify Areas for Improvement:

- Once you’ve tracked your finances, you can identify areas where you can cut back. This could mean reducing unnecessary spending or paying off high-interest debts.

2. Create a Budget

Creating a budget is one of the most powerful tools you have to achieve financial freedom. A budget helps you control your spending, save more, and invest wisely. Here’s how to create a budget that works for you:

- Set Clear Financial Goals:

- Decide what you want to achieve with your money. For example, saving for a house, building an emergency fund, or investing for retirement.

- Decide what you want to achieve with your money. For example, saving for a house, building an emergency fund, or investing for retirement.

- The 50/30/20 Rule:

- A simple and effective budgeting method is the 50/30/20 rule:

- 50% for needs (housing, groceries, utilities)

- 30% for wants (entertainment, dining out)

- 20% for savings and investments

- A simple and effective budgeting method is the 50/30/20 rule:

- Automate Your Savings:

- Set up automatic transfers to your savings or investment accounts. This ensures you are consistently putting money aside without having to think about it.

3. Build an Emergency Fund

One of the most important steps to achieving financial freedom is having a safety net. An emergency fund can protect you from financial setbacks, such as medical bills, car repairs, or sudden job loss.

- How Much Should You Save? Ideally, you should aim to save 3-6 months of living expenses in your emergency fund. This amount will give you enough cushion to weather any financial storms that may come your way.

4. Get Rid of High-Interest Debt

Debt can be a major roadblock on your path to financial freedom. Especially high-interest debt, such as credit card debt or payday loans. The longer you hold on to this debt, the more money you’ll pay in interest.

- Pay Off High-Interest Debt First:

- Focus on paying off high-interest debts as quickly as possible. Consider using the debt snowball method (paying off the smallest debts first) or the debt avalanche method (paying off high-interest debts first).

- Focus on paying off high-interest debts as quickly as possible. Consider using the debt snowball method (paying off the smallest debts first) or the debt avalanche method (paying off high-interest debts first).

- Avoid Accumulating New Debt:

- Once your debts are paid off, avoid taking on new high-interest debts. Use cash or debit cards instead of credit cards when possible.

5. Save and Invest for the Future

Saving money is important, but investing it is what truly helps you build wealth over time. Investments can generate passive income, allowing you to grow your money without actively working for it.

- Start with Low-Risk Investments:

- If you’re new to investing, start with low-risk options like Public Provident Fund (PPF), Fixed Deposits (FDs), or Sukanya Samriddhi Yojana.

- If you’re new to investing, start with low-risk options like Public Provident Fund (PPF), Fixed Deposits (FDs), or Sukanya Samriddhi Yojana.

- Explore Equity Investments:

- Once you’re comfortable, consider investing in stocks, mutual funds, or exchange-traded funds (ETFs). These offer higher returns but come with greater risk.

- Once you’re comfortable, consider investing in stocks, mutual funds, or exchange-traded funds (ETFs). These offer higher returns but come with greater risk.

- Consider Real Estate:

- Investing in property is another way to build wealth. In India, real estate can be a good long-term investment, especially in rapidly growing cities.

- Investing in property is another way to build wealth. In India, real estate can be a good long-term investment, especially in rapidly growing cities.

- Retirement Planning:

- Ensure that you are contributing towards a retirement plan, such as the Employees’ Provident Fund (EPF) or National Pension Scheme (NPS), to ensure that you are financially independent in your later years.

6. Diversify Your Income Sources

One of the key principles of financial freedom is having multiple sources of income. Relying on a single paycheck or business income can be risky, especially in uncertain economic times.

- Side Hustles:

- Consider starting a side business or freelancing. This can be anything from online tutoring to starting an e-commerce store or becoming a freelance writer.

- Consider starting a side business or freelancing. This can be anything from online tutoring to starting an e-commerce store or becoming a freelance writer.

- Invest in Passive Income Streams:

- Look for opportunities to earn passive income, such as renting out property, earning dividends from stocks, or starting a blog or YouTube channel.

- Look for opportunities to earn passive income, such as renting out property, earning dividends from stocks, or starting a blog or YouTube channel.

- Build an Online Presence:

- In today’s digital age, creating an online presence can be a lucrative source of income. Whether it’s affiliate marketing, selling products, or offering services, there are numerous opportunities to earn money online.

7. Stay Consistent and Stay Disciplined

Achieving financial freedom is not a one-time task; it’s a continuous process. Consistency and discipline are key to making progress. Stay committed to your financial goals, review your budget regularly, and make adjustments as necessary.

- Track Your Progress:

- Regularly check your financial progress to ensure you’re staying on track.

- Regularly check your financial progress to ensure you’re staying on track.

- Stay Patient:

- Financial freedom doesn’t happen overnight. Stay patient and persistent, and keep working

- towards your goals.

8. Keep Learning, Stay Updated on Finance

The world of finance is moving/changing fast. Markets shift, policies change, and new investment tools pop up regularly. Staying updated means you can make smarter decisions, avoid outdated advice, and stay ahead of financial trends. Whether it’s through reading trusted financial news, taking online courses, or listening to expert-led podcasts, lifelong learning is your financial edge.

9. Maintain properties/Spaces

Real estate isn’t just about owning land; it’s also about creating opportunities. From renting out a spare room to managing multiple units, your properties can generate consistent income with the right upkeep. Regular maintenance not only preserves value but also attracts better tenants and minimizes costly repairs. Think of it as protecting your income stream while your property value grows.

10. Always have a Financial Advisor

Even the smartest investors need a second opinion. A trusted financial advisor helps you build a strategy, manage risk, and plan for long-term goals. They bring objectivity to emotional decisions and insights you might miss on your own. Whether it’s retirement planning, tax strategy, or investment diversification, having an expert in your corner can make all the difference.

Dream Financial Freedom: Some Practical Tips for Indians

Here are some practical tips tailored for Indian readers to achieve financial freedom:

- Start Early: The power of compounding works best when you invest early. Even small investments can yield significant returns over time.

- Tax Savings: Take advantage of tax-saving instruments like ELSS, PPF, and National Pension Scheme (NPS) under Section 80C.

- Invest in SIPs: Systematic Investment Plans (SIPs) in mutual funds are a disciplined way to grow your wealth gradually.

- Side Income: Explore side hustles or freelancing opportunities to boost your income.

- Live Below Your Means: Avoid lifestyle inflation. Focus on saving and investing rather than spending unnecessarily.

- Health Insurance: Protect yourself and your family with comprehensive health insurance to avoid unexpected medical expenses.

By following these structured strategies and using the right tools, you can make informed decisions and steadily progress toward financial freedom 2025.

Click to Download:-

How Much Retirement Savings Do You Need Each Year?

The amount of retirement savings you’ll need each year depends on several key factors, including your lifestyle, retirement age, life expectancy, health, and other sources of income (like Social Security or a pension). However, a common rule of thumb can help you estimate your annual needs:

1. The 4% Rule (General Estimate)

This rule suggests you can withdraw 4% of your total retirement savings each year, adjusted for inflation, and have a high probability of not running out of money over 30 years.

- For example: If you want $50,000 per year from your savings: 50,0000.04=1,250,000\frac{50,000}{0.04} = 1,250,0000.0450,000=1,250,000 You’d need about $1.25 million in retirement savings.

2. Personalizing Your Retirement Needs

Here’s how you can tailor the estimate:

- 🌍 Lifestyle: Do you plan to travel often or live modestly?

- 🏡 Housing: Will your mortgage be paid off? Will you downsize?

- 💵 Other Income: Subtract Social Security, pensions, annuities, or part-time work from your annual spending need.

- 📆 Retirement Duration: Plan for 30 years or more, especially if you retire early or have a family history of longevity.

- 📈 Inflation: Factor in that your spending power will decline unless your withdrawals increase over time.

3. Quick Formula to Estimate Savings Needed

Annual Spending Need=Total Expected Spending−Guaranteed Income

Best Apps for Financial Planning

In today’s digital age, managing your finances has become easier with mobile apps. Here are some of the best apps for financial planning in India:

- Mint: A popular app for tracking expenses and creating budgets.

- Moneycontrol: Ideal for tracking investments and stock market updates.

- ET Money: Helps with expense tracking, investment management, and tax-saving plans.

- Scripbox: Provides investment guidance and helps manage mutual funds.

- Groww: A user-friendly app for investing in stocks, mutual funds, and fixed deposits.

Tools for Financial Freedom

Utilizing the right financial freedom tools can help you make better decisions and stay on track toward financial freedom:

- Budget Planners: Online tools like Google Sheets and budgeting apps to track expenses.

- Investment Calculators: Use SIP calculators, retirement calculators, and EMI calculators for precise financial planning. These are financial freedom calculators.

- Tax Planning Tools: Platforms like ClearTax and the Income Tax Department’s official website can simplify tax filing.

- Net Worth Tracker: Track your assets and liabilities using apps like Personal Capital.

- Financial Advisor Services: Consider Robo-advisors like Zerodha Varsity for investment education.

By understanding both financial independence and financial freedom, you can better plan your financial future and work towards a life where money empowers rather than restricts you.

What is the FIRE Number & How to Calculate It?

The FIRE number (Financial Independence, Retire Early) refers to the total amount of money you need to save and invest in order to live comfortably without relying on active income. It represents the size of your investment portfolio that can generate enough passive income to cover your annual living expenses.

How to Calculate Your FIRE Number

To calculate your FIRE number India, follow these steps:

- Estimate Your Annual Expenses: Determine how much money you need each year to maintain your current lifestyle.

- Apply the 4% Rule: This rule assumes you can safely withdraw 4% of your portfolio annually without depleting your savings.

- Multiply Your Annual Expenses by 25: Since 1 divided by 0.04 equals 25, this gives you the investment amount required.

Example:

If your annual expenses are ₹8,00,000, then:

₹8,00,000 × 25 = ₹2,00,00,000 (₹2 crores)

This means your FIRE number is ₹2 crores. Once your investments reach this level, you can rely on them to cover your expenses, achieving financial freedom.

Conclusion

Financial freedom in India requires more than just saving; it demands a strategic blend of budgeting, debt management, smart investing, and diversifying income sources. Building an emergency fund, using tax-saving tools, and planning for retirement are essential pillars. The 4% withdrawal rule and the FIRE number help quantify your goals, while staying disciplined and continuously learning ensures long-term success. With patience and consistency, anyone can break free from paycheck dependency and enjoy true financial independence, living life on their own terms with peace of mind and security.

Approach Chegg India Expert Hiring and gain some knowledge of the corporate world.

Recommended Read:-

- Investment Options: Top 15 Picks for 2025

- How to Start a Startup in India

- Top 10 Captcha Entry Jobs in India for Daily Earnings (2025)

- 30 Best Refer and Earn Apps in India (2025) – Earn Money Online!

Frequently Asked Questions (FAQ’s)

What is meant by financial freedom?

Financial freedom means having enough passive income (rentals, dividends, etc.) or savings to cover your lifestyle without relying on a 9-to-5 job. Example: Retiring early or living off investments.

What are the 7 steps to financial freedom?

1. Track expenses (budgeting apps like Mint).

2. Build an emergency fund (3–6 months of expenses).

3. Pay off high-interest debt (credit cards, loans).

4. Invest consistently (stocks, mutual funds, real estate).

5. Diversify income (side hustles, freelancing).

6. Plan for retirement (401(k), NPS, or PPF).

7. Protect wealth (insurance, estate planning).

What is the 4% rule of financial freedom?

The 4% rule states you can withdraw 4% of your savings yearly in retirement without running out of money. Example: ₹5 crore savings = ₹20 lakh/year. Based on the Trinity Study.

What is total financial freedom?

Total financial freedom means having zero financial stress and unlimited choices (e.g., traveling, philanthropy) thanks to substantial wealth exceeding your needs.

What is the financial freedom pyramid?

A step-by-step wealth-building framework:

1. Base: Emergency fund + debt-free.

2. Mid: Stable income + investments.

3. Top: Passive income > expenses

What is the Financial Freedom Formula?

The 25x Rule is a popular formula: Save 25 times your annual expenses. Example: If you spend ₹10 lakh/year, aim for ₹2.5 crore in investments. Withdraw 4% yearly (per the 4% rule) to sustain your lifestyle.

Steps to Apply the Formula:

1. Calculate yearly expenses.

2. Multiply by 25 for your target savings.

3. Invest in income-generating assets (stocks, real estate).

What are the best financial freedom books?

Top reads:

1. “Rich Dad Poor Dad” by Robert Kiyosaki (mindset shift).

2. “The Simple Path to Wealth” by JL Collins (index fund investing).

3. “Your Money or Your Life” by Vicki Robin (FI/RE movement).

4. “The Millionaire Next Door” by Thomas Stanley (wealth habits).

5. “I Will Teach You to Be Rich” by Ramit Sethi (practical finance).

What are the best Financial Freedom Quotes?

1. “Live like no one else now, so later you can live like no one else.” – Dave Ramsey

2. “Financial freedom is freedom from fear.” – Robert Kiyosaki

3. “Do not save what is left after spending; spend what is left after saving.” – Warren Buffett

4. “The goal isn’t more money. The goal is living life on your terms.” – Unknown

5. “Invest in yourself. Your career is the engine of your wealth.” – Grant Cardone

What is your financial freedom?

Financial freedom is the ability to make life choices without being constrained by money considerations. It goes beyond just having a comfortable income; it embodies the power to live life on your terms, pursuing dreams, and finding peace of mind through a secure financial foundation.

Is it possible to attain financial freedom on a limited income?

Yes, financial freedom is achievable with low income by budgeting wisely, saving consistently, investing smartly, and increasing income streams over time. Discipline and smart planning are key to long-term success.

What are the main challenges to achieving financial freedom?

Major obstacles include poor money management, high debt, lack of savings, inconsistent income, and limited financial knowledge. Overcoming these requires discipline, education, and a clear financial plan.

Why is having a financial advisor important?

A financial advisor provides expert guidance on investments, tax planning, and retirement strategies. They help you avoid costly mistakes and create a personalized roadmap to achieve financial independence faster.