Gratuity is a financial reward given by employers to employees as appreciation for long-term service. Governed by the Payment of Gratuity Act, 1972, it is mandatory for companies with 10 or more employees in India. If you’re wondering how to calculate gratuity in India, this easy guide explains the entire process, step by step. From eligibility rules to the gratuity calculation formula, we’ll help you understand how much you’re entitled to receive and how to compute it effortlessly. Whether you’re planning your exit or retirement, this guide ensures you don’t leave your hard-earned money on the table.

What is Gratuity?

Gratuity is a lump-sum payment made by an employer to an employee when they retire, resign, or are terminated after completing a minimum service period. It is a reward for long-term dedication and loyalty to the organization.

In India, gratuity eligibility is mandatory under the Payment of Gratuity Act if the following conditions are met:

- The employee has worked for at least five years in the organization.

- The organization employs 10 or more people.

However, there are exceptions. For instance, if an employee passes away or becomes disabled due to illness or accident, gratuity can be paid even before completing five years of service.

Now that you know what gratuity is, let’s move on to how to calculate gratuity in India under the law.

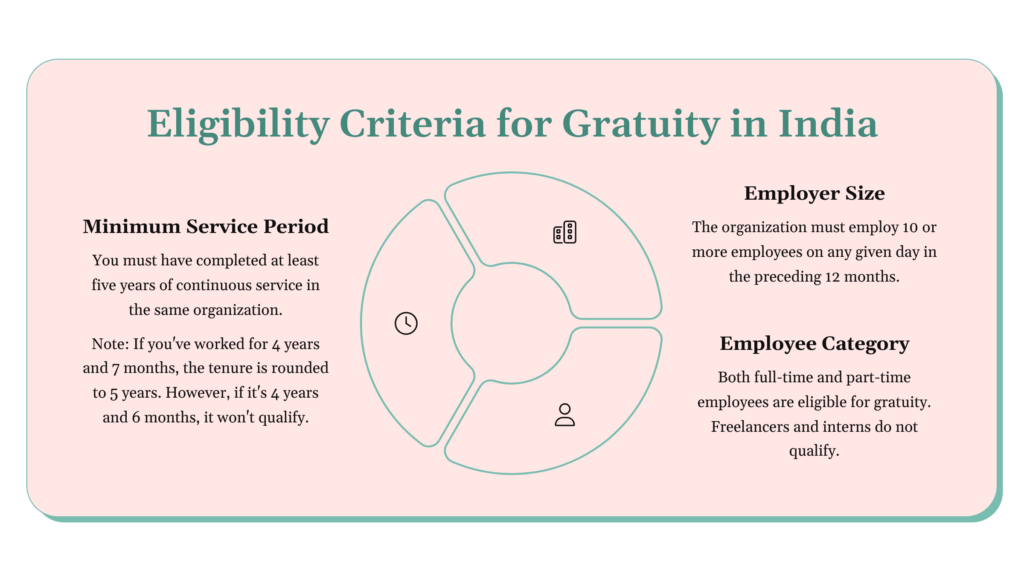

Eligibility Criteria for Gratuity in India

To claim gratuity, certain conditions must be fulfilled. Here’s a breakdown of who qualifies for gratuity:

- Minimum Service Period:

- You must have completed at least five years of continuous service in the same organization.

- Note: If you’ve worked for 4 years and 7 months, the tenure is rounded to 5 years. However, if it’s 4 years and 6 months, it won’t qualify.

- Employer Size:

- The organization must employ 10 or more employees on any given day in the preceding 12 months.

- The organization must employ 10 or more employees on any given day in the preceding 12 months.

- Employee Category:

- Both full-time and part-time employees are eligible for gratuity. Freelancers and interns do not qualify.

If you meet these criteria, you’re eligible to receive gratuity. Now, let’s explore the formula for how to calculate the gratuity based on your salary and years of service.

The Formula for Gratuity Calculation

The calculation of gratuity in India depends on whether your organization is covered under the Payment of Gratuity Act. To estimate your payout, you can use the gratuity calculation India formula, which considers the last drawn salary and years of service. Below is the formula used to calculate gratuity:

For Organizations Covered Under the Payment of Gratuity Act

If your employer falls under the ambit of the Payment of Gratuity Act, the gratuity amount is calculated using the following formula:

Gratuity = (Basic Salary + Dearness Allowance) × 15 ÷ 26 × Tenure of Service

Here’s what each component means:

- Basic Salary: Your fixed monthly salary, excluding allowances like HRA, conveyance, etc.

- Dearness Allowance (DA): An allowance provided to offset the impact of inflation.

- 15/26: This represents 15 days of salary for every year of service.

- Tenure of Service: Total number of years worked in the organization.

Steps to Calculate Gratuity:

- Use this formula

Gratuity = (15 × last drawn basic salary × years of service) ÷ 26

(15 days’ salary for every completed year of service, divided by 26 working days) - Identify your components

- Basic salary + Dearness Allowance (DA) = Last drawn salary

- Round down the number of years of service (e.g., 7 years 10 months = 7 years)

- Example

- Last drawn salary = ₹30,000

- Years of service = 10

- Gratuity = (15 × 30,000 × 10) ÷ 26 = ₹1,73,077 approx.

- Tax exemption

Example Calculation

Let’s say your basic salary is ₹40,000 per month, DA is ₹10,000, and you’ve worked for 8 years and 7 months.

- Add Basic Salary and DA: ₹40,000 + ₹10,000 = ₹50,000

- Multiply by 15÷26: ₹50,000 × 15÷26 = ₹28,846 (monthly gratuity)

- Multiply by tenure: ₹28,846 × 8.5 years = ₹2,45,191

So, your gratuity payout would be approximately ₹2,45,191.

For Organizations Not Covered Under the Act

If the Payment of Gratuity Act doesn’t cover your employer, the formula changes slightly:

Gratuity = Average Salary × ½ × Tenure of Service

Here, the Average Salary is the average of your last 10 months’ salary.

How to Calculate Gratuity for Different Types of Employees?

The method of calculating an employee’s gratuity varies depending on the type of employment. Whether you are a government employee, a private sector employee, or a daily wage worker, understanding your gratuity calculation is crucial to ensure you receive the correct amount.

Let’s explore how gratuity is calculated for different categories of employees.

1. How to Calculate Gratuity for Government Employees

Government employees in India are entitled to gratuity as per the Payment of Gratuity Act, 1972. The calculation method is as follows:

Formula for Government Employees:

Gratuity = (Last Drawn Salary × 15 × Number of Years Worked) ÷ 26

Where:

- Last Drawn Salary includes Basic Salary + Dearness Allowance (DA)

- 15 represents 15 days of salary per completed year of service

- 26 represents the number of working days in a month

Key Features of Gratuity for Government Employees:

- The maximum gratuity amount an employee can receive is ₹20 lakh.

- 100% tax-free, meaning there are no deductions on the gratuity amount.

- No limit on years of service – the gratuity amount increases based on tenure.

Example Calculation:

If a government employee’s last drawn salary (Basic + DA) is ₹50,000, and they have worked for 30 years, the gratuity calculation will be:

(50,000 × 15 × 30) ÷ 26 = ₹8,65,385

Since this amount is below the ₹20 lakh limit, it remains fully tax-free.

For government employees, how calculate the gratuity is straightforward as it follows a fixed structure with complete tax exemption.

2. How to Calculate Gratuity for Private Sector Employees

Private sector employees also receive gratuity if they have completed at least five years of continuous service with the same employer. The formula used is the same as for government employees.

Formula for Private Sector Employees:

Gratuity = (Last Drawn Salary × 15 × Number of Years Worked) ÷ 26

Key Features of Gratuity for Private Sector Employees:

- The maximum gratuity amount is ₹20 lakh.

- Tax exemption is available only up to ₹20 lakh. Any amount exceeding ₹20 lakh is taxable as per the income tax slabs.

- If the company is not covered under the Gratuity Act, they may use 30 days instead of 26 days for calculation.

Example Calculation:

If a private sector employee has a last drawn salary of ₹70,000 and has worked for 25 years, the gratuity amount will be:

(70,000 x 15 x 25) ÷ 26 = ₹10,09,615

Since this amount is below ₹20 lakh, it is fully tax-free. However, if the gratuity amount exceeds ₹20 lakh, the excess portion is taxable.

For private sector employees, understanding how companies calculate gratuity helps in tax planning and financial decision-making.

3. How to Calculate Gratuity for Daily Wage Workers

Unlike salaried employees, daily wage workers do not have a fixed monthly salary. Instead, their gratuity is calculated based on their daily wage rate.

Formula for Daily Wage Workers:

Gratuity = ( Daily Wage × 15 ) × Number of Years Worked

Where:

- Daily Wage is the average daily earnings of the worker

- 15 represents 15 days of salary per completed year of service

Key Features of Gratuity for Daily Wage Workers:

- The worker must have completed at least five years of service with the same employer.

- The employer should be covered under the Gratuity Act 1972 for this benefit to apply.

- The maximum gratuity amount is ₹20 lakh, and any excess is taxable.

Example Calculation:

If a daily wage worker earns ₹800 per day and has worked for 10 years, their gratuity amount will be:

( 800 × 15 ) × 10 = ₹1,20,000

This amount is well within the tax-free limit of ₹20 lakh.

Knowing how to calculate gratuity ensures that daily wage workers know their rightful benefits and can claim them accordingly.

Gratuity serves as a financial security measure for employees after long-term service. Whether you are a government employee, a private sector employee, or a daily wage worker, understanding how to calculate gratuity is essential to ensure you receive the correct amount.

By following the right formula and keeping track of tax implications, you can maximize your gratuity benefits and plan for a secure financial future.

What Can a Gratuity Calculator Do for You?

A gratuity calculator can be incredibly helpful for the following reasons:

- Accurate Calculations: It ensures you get an accurate estimate of the gratuity amount you’re entitled to, based on your salary and years of service.

- Time-Saving: Quickly computes the amount without manual calculations, saving you time and effort.

- Financial Planning: Helps you plan your finances better by giving you a clear idea of the gratuity you can expect upon retirement or job change.

- Compliance: Ensures that calculations are in line with local laws and regulations, reducing the risk of errors.

- Transparency: Provides clear and transparent information, helping you understand how the gratuity amount is derived.

Tax Implications of Gratuity in India

Gratuity is tax-free up to ₹20 lakhs for government employees and certain categories of private employees.

Taxation Rules for Gratuity in India

1. For Government Employees:

If you are a central or state government employee, your entire gratuity amount is 100% tax-free, regardless of how much you receive.

2. For Private Sector Employees:

The tax implications of gratuity for private employees depend on the amount received:

- If the gratuity amount is ₹20 lakhs or less, it is completely tax-free.

- If the gratuity amount is more than ₹20 lakhs, the excess amount is taxed as per your income tax slab.

3. For PSU and other semi-government employees,

tax treatment depends on whether their employer is classified under the Act. Any amount above the exempt limit is taxable under “Income from Salary.”

Example of Gratuity Tax Calculation

Let’s say an employee from the private sector receives ₹25 lakhs as gratuity.

- The first ₹20 lakhs is tax-free.

- The remaining ₹5 lakhs will be added to the employee’s income and taxed based on the applicable income tax slab.

- If the employee falls under the 30% tax slab, they will have to pay ₹1.5 lakhs (30% of ₹5 lakhs) as tax on the gratuity amount exceeding ₹20 lakhs.

How to Calculate Gratuity and Plan for Taxes?

Understanding how to calculate gratuity can help employees plan their finances better. Employees can also reduce tax liability by using exemptions available under the Income Tax Act or investing in tax-saving options.

By knowing these taxation rules, employees can be better prepared to handle their gratuity payouts effectively.

Read More:- How to Calculate HRA in Salary

How to Claim Gratuity?

Knowing how to calculate gratuity amount and the process to claim it can help employees receive their rightful amount without any hassle. Below are the steps to claim gratuity in India:

1. Submit a Gratuity Application (Form I)

Employees who are eligible for gratuity must fill out Form I and submit it to their employer. This form serves as an official request for the gratuity payment. It should include details such as:

- Employee’s name and address

- Name and address of the employer

- Date of joining and date of leaving the company

- Total number of years worked

- Last drawn salary

2. Employer Verifies Eligibility and Calculates Gratuity Amount

Once the application is submitted, the employer will verify whether the employee meets the eligibility criteria. Employees can also learn how to calculate gratuity using the standard formula.

3. Payment is Processed Within 30 Days

Once the gratuity amount is calculated, the employer must process the payment within 30 days from the date of application submission. The payment can be made through bank transfer, cheque, or demand draft.

4. Interest on Delayed Payments

If the employer fails to pay gratuity within 30 days, they are legally bound to pay interest on the pending amount as per government rules. This ensures that employees receive their gratuity without unnecessary delays.

Knowing how to calculate gratuity of an employee and understanding the proper claiming procedure ensures that employees receive their rightful benefits without delays. By following a clear step-by-step process, individuals can enjoy a smooth and stress-free experience when claiming their gratuity payout.

Common Mistakes And How To Avoid Them?

Employers are responsible for calculating the gratuity amount. And then pay it to their employees in a timely and accurate manner. Yet, mistakes can happen, and employers need to be aware of these common errors to avoid them. Here are some common mistakes and how to avoid them:

- Incorrect Calculation of Service Period:

- Employers should ensure that they include all the years of service, including the fractional years, when calculating the gratuity amount.

- Employers should ensure that they include all the years of service, including the fractional years, when calculating the gratuity amount.

- Not Considering Basic Salary:

- Gratuity is calculated based on the employee’s last drawn salary, which includes the basic salary and dearness allowance. Employers sometimes don’t include the DA along with the base salary, which can result in an incorrect calculation of the gratuity amount.

- Gratuity is calculated based on the employee’s last drawn salary, which includes the basic salary and dearness allowance. Employers sometimes don’t include the DA along with the base salary, which can result in an incorrect calculation of the gratuity amount.

- Ignoring Changes in Salary:

- Employers should consider all employee salary changes while calculating the gratuity amount. For example, the employer must consider a hike given during the service period. That is how gratuity is calculated.

- Employers should consider all employee salary changes while calculating the gratuity amount. For example, the employer must consider a hike given during the service period. That is how gratuity is calculated.

- Not Maintaining Accurate Records:

- Employers should maintain accurate records, including the employee’s service period and salary details. Incomplete records can result in an incorrect calculation of the gratuity amount.

- Employers should maintain accurate records, including the employee’s service period and salary details. Incomplete records can result in an incorrect calculation of the gratuity amount.

- Delay in Payment:

- Employers should ensure that the gratuity amount is paid. This will be paid within 30 days of the employee’s last working day. Payment delays can result in penalties and legal issues.

Tips to Maximize Your Gratuity Payout

To ensure you receive the maximum gratuity amount, follow these tips:

- Stay Updated on the Rules:

- Keep track of changes in the Payment of Gratuity Act.

- Negotiate Salary Components:

- Ensure your basic salary and DA are higher, as these directly impact gratuity calculations.

- Maintain Proper Records:

- Keep documents like appointment letters, salary slips, and resignation letters safe.

- Seek Professional Help:

- Consult a tax advisor if you’re unsure about tax exemptions or calculations.

These strategies will help you maximize your gratuity payout while ensuring compliance with legal requirements.

Conclusion

Understanding how to calculate gratuity is essential for every working professional in India. By following the steps outlined in this guide, you can accurately determine your gratuity amount and avoid unnecessary complications. Remember, gratuity is not just a financial benefit—it’s a reward for your hard work and dedication.

Share this article with your friends and colleagues if you found it helpful. For quick calculations, use our free gratuity calculator tool available on our website.

Want to explore helpful techniques to save and grow your hard-earned money? Dive into our guide on Earn Online.

Read More:

- What Is Variable Pay in CTC: Do Incentives Matter?

- Top 20 Powerful Self-Employment Ideas in India [2025]

- Gross Salary Explained: Meaning, Composition, Calculation

- Top Captcha Typing Jobs in 2025: Earn Daily with Zero Investment

Frequently Asked Questions (FAQs)

What is the formula for calculating gratuity?

The formula for calculating gratuity is:

Gratuity = (Last Drawn Salary x 15 x Years of Service) / 26

This formula is for employees covered under the Gratuity Act in India.

How much is gratuity after 5 years?

After 5 years of service, an employee is typically eligible for gratuity, which is calculated as 12 times the last drawn basic salary plus dearness allowance (DA), according to the Payment of Gratuity Act. The formula for calculating gratuity is: (15/26) * [Last drawn salary (Basic + DA)] * Number of years of service.

How to calculate a 20% tip?

To calculate a 20% tip, multiply the total bill amount by 0.20. For example, if the bill is ₹1,000: ₹1,000 \times 0.20 = ₹200.

What is 15 in the gratuity calculation?

The number 15 represents the 15 days of salary for each year of service, as per the Gratuity Act.

How is gratuity calculated, 26 or 30?

The gratuity calculated is 26. The formula is “Gratuity = (15/26) x Last Drawn Salary x (Number of Completed Years of Service) x 240/365.”

Is gratuity calculated on basic salary?

Yes, gratuity is calculated based on the employee’s last drawn basic salary and dearness allowance (DA). The formula is:

“Gratuity = (15/26) x Last Drawn Salary x (Number of Completed Years of Service) x 240/365”.

How can we calculate gratuity manually?

To calculate gratuity manually:

1. Formula: “Gratuity = (15/26) x Last Drawn Salary x (Number of Completed Years of Service) x 240/365”

2. Steps:

i) Identify the last drawn basic salary & DA.

ii) Multiply by 15 (days).

iii) Multiply by years of service.

iv) Divide by 26 (working days in a month).

Who is eligible for gratuity?

Employees with at least 5 years of continuous service in a company with 10+ employees.

Is gratuity applicable for contract workers?

Usually no, unless the contract terms or company policy provide for it.

How much gratuity (%) is deducted from the salary?

Under the Payment of Gratuity Act, 1972, gratuity is calculated as 4.81% of the Basic Pay.

Will I get gratuity if I resign?

Generally, you are eligible for gratuity after completing five years of continuous service with an employer. Resigning before this period means you typically will not receive gratuity, except in cases involving death or disability. If you have worked for more than 4 years and 240 days, some sources say you may be eligible for gratuity, as this is considered equivalent to 5 years of service.

Is gratuity taxable?

For government employees: Fully tax-free, regardless of the amount.

For private sector employees: Tax-free up to ₹20 lakh; excess is taxable as per income tax slabs.